Effective November 9, 2020, the Securities and Exchange Commission (SEC) amended its disclosure requirements related to human capital resources (HCR). This was the first significant revision to SEC filing rules in over 30 years.

“The final rules require the following disclosures to the extent they are material to the understanding of the registrant’s business as a whole:

- A description of the registrant’s human capital resources, including the number of persons employed by the registrant, and

- Any human capital measures or objectives that the registrant focuses on in managing the business, potentially including measures or objectives that address the development, attraction, and retention of personnel.” (1)

The final rules were purposefully vague to allow companies “flexibility to tailor their disclosures to their unique circumstances, using some or all of the components of any current or future standard or framework to help the reader understand the registrant’s business, financial condition, and prospects through the lens used by management and the board of directors to manage and assess the company’s performance.” (1)

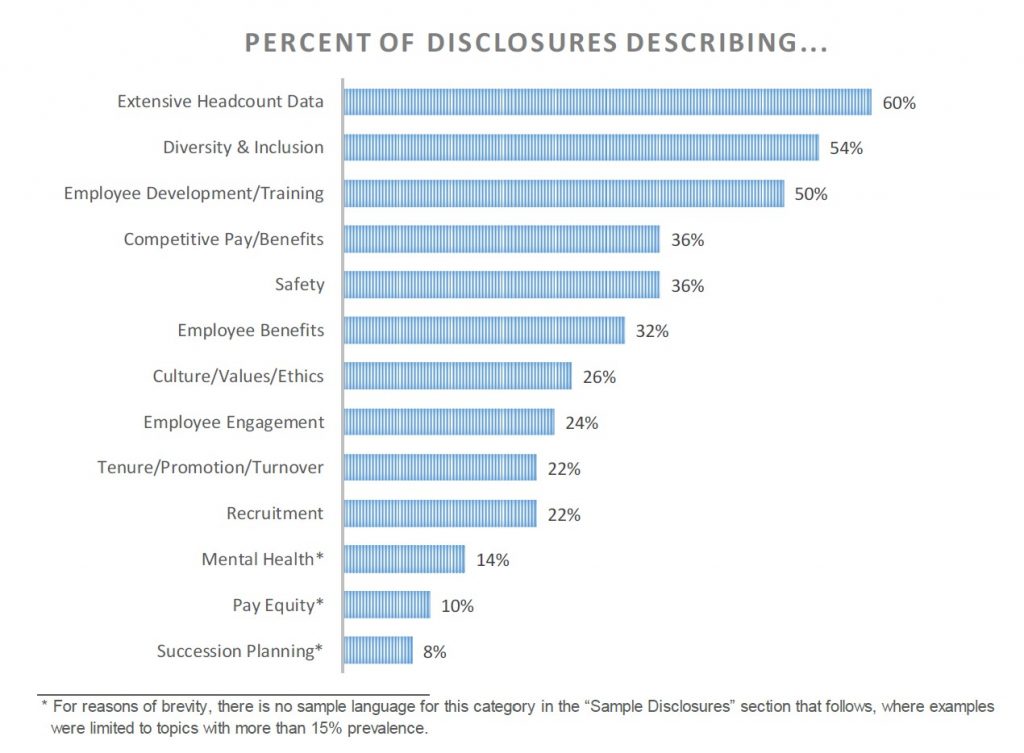

The consulting firm FW Cook conducted a review of the first 50 Form 10-K’s filed by large companies (more than $1 billion in market capitalization) (2). Unsurprisingly, the results revealed a wide range of disclosures on human capital resources (HCR). The length of the disclosures ranged from 9 words to 1582 words, with a median of 369 words. The mid-range (25th to 75th percentile) was 205 words to 601 words.

Some companies concluded that development, attraction, and retention of personnel etc. were normal and did not require additional disclosures. Others reference documents, such as their corporate responsibility or proxy statements, etc.

In their analysis, FW Cook identified the 13 most common categories of disclosure under HCR, which are shown on the chart below. Their report includes sample language pulled from numerous Form 10-K’s. The disclosures are mostly narratives, sometimes with a small amount of data.

Conclusion

The SEC human capital resource disclosure requirement follows on the heels of ISO 30414:2018 (Human resource management — Guidelines for internal and external human capital reporting), which was adopted two years ago. In this age of transparency, the requirements for HCR disclosure will grow, which increases the importance of having an HR system that can analyze data across multiple variables. Disclosing the first cut of data from an HR system could have harmful results.

Contact Auxillium HRnetSource to find out more about our powerful HR analysis tools.