Why your use-it-or-lost it PTO policy isn’t working

The pandemic has disrupted employees’ summer vacation and travel plans. In addition, employees just getting back to the office may be reluctant to schedule time off, either because they have a lot to do or because they don’t want to be seen as dispensable.

The pandemic has disrupted employees’ summer vacation and travel plans. In addition, employees just getting back to the office may be reluctant to schedule time off, either because they have a lot to do or because they don’t want to be seen as dispensable.

Warning: You’ll run head long into a Payroll and HR catastrophe if you have a use-it-or-lose-it PTO policy.

Reason No. 1: Some employees are probably sitting on a huge pot of time off, which can translate into staffing shortages at the end of the year as employees rush to use their time, rather than lose it.

Reason No. 2: But it’s not just staffing issues. Consider the money. You may take a huge financial hit if you have to pay out the value of employees’ accrued time upon termination or if you cash employees out at the end of the year.

PTO possibilities

One of the negative aspects about working from home is you can always work. Then you burn out. If you don’t want your employees sacking out on the couch to binge watch TV (which can lead to another sort of burn out), communicating with them about taking time off this year is essential. You have options:

- Encourage employees to take long weekends

- Encourage employees to work partial days

- Encourage employees to take mental health days

- Work with employees to develop personal PTO plans

- Require employees to take a certain number of days off before Labor Day.

PTO policy choices

PTO options notwithstanding, now may be the perfect time to take a critical look at your PTO plan. Your policy choices are pretty clear:

- You can allow employees to roll over their unused time. Downside: You have to avoid employees building up a giant bank of time off.

- You can cap the amount of time you will allow employees to roll over. Excess time can be cashed out or forfeited, but whether accrued time can be forfeited depends on state law.

- Provided state law allows, PTO time not used by the end of the year can be forfeited. But that’s not the best move for employee morale these days.

PTO and payroll

The issue for Payroll and executives who are thinking of changing the company’s PTO policy is taxing the value of leave. You have three choices:

- When employees earn it

- When they roll it over

- When they take time off.

The correct approach depends on whether accrued leave is subject to the rules of constructive receipt—an issue Payroll pros know well.

Constructive receipt is a tax timing issue. In addition to withholding when employees are actually paid, constructive receipt requires you to withhold when wages are constructively paid—that is, when wages are credited to the account of, or set apart for, employees so they can draw on them at any time.

In keeping with the rule of constructive receipt, the IRS has consistently concluded the value of accrued leave is taxable to all employees when it’s earned, regardless of when or even whether employees take leave. Here’s how this plays out.

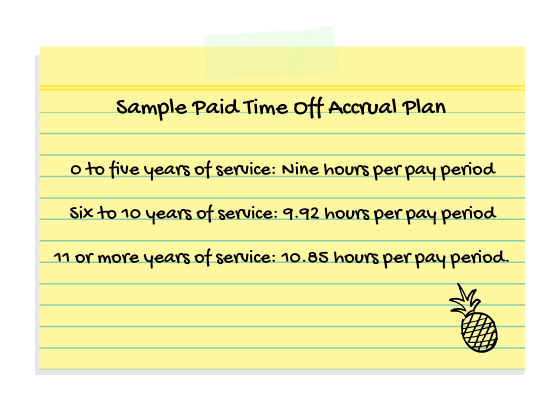

Example: Sparky’s PTO plan allows employees to accrue annual leave as follows:

- 0 to five years of service: Nine hours per pay period

- Six to 10 years of service: 9.92 hours per pay period

- 11 or more years of service: 10.85 hours per pay period.

Under Sparky’s plan, employees can carry over their accrued annual leave into the next year, but on Dec. 31, employees can’t have more than 480 hours of leave in their banks. Excess hours are cashed out. In addition, employees may make written requests to cash out their time. Accrued leave is cashed out when employees terminate.

Result: Since employees aren’t restricted from cashing out their accrued leave, accruals are taxable to all employees as they are credited to their accounts, regardless of whether they take leave.

To get out from under constructive receipt, you must throw a substantial roadblock in the way of employees’ elections. You can do this by following the basic cafeteria plan rule of requiring employees to irrevocably choose during the preceding year whether they’ll roll over their unused leave or cash it out during the next year.

Once the roadblock is set up, employees will be taxed on the value of their leave when they take it or cash out. Employees who don’t take leave aren’t taxed.

Lesson learned: If you’re going to change your PTO plan, do it on a prospective basis to avoid constructive receipt issues.