What are Starter 401(k) plans?

There’s never been a better time for employers to start a new 401(k). Why, you might ask?

Recent retirement legislation has made offering a 401(k) more affordable than ever. Thanks to the SECURE 2.0 Act, eligible employers may receive up to $16,500 in tax credits¹ over a plan’s first three years to help offset initial plan costs. The Act also introduced the Starter 401(k) plan, a retirement benefit designed to make it easier for businesses to give its employees a way to save for the future.

In this post, we’ll break down everything employers need to know about Starter 401(k) plans, including:

- What is a Starter 401(k)?

- How do Starter 401(k) plans work?

- Who is eligible for a Starter 401(k) plan?

- What's the difference between a standard and a Starter 401(k) plan?

Read on to learn more and determine if a Starter 401(k) plan is right for you.

What are Starter 401(k) plans?

Think of a Starter 401(k) as a simplified employer-sponsored retirement plan with lower saving limits than a standard 401(k). These plans help employers offer a retirement benefit by streamlining two of the most significant barriers when it comes to offering retirement savings plans: cost and ease of administration.

Starter 401(k) plans were established under the SECURE 2.0 Act, which was signed into law in 2022. The need for retirement reform is significant and has bipartisan support. Data shows that 56% of Americans are worried about not having a financially secure retirement, and 65% worry they’ll have to work past retirement age to have enough money to retire.

The SECURE 2.0 act aims to positively impact these statistics. According to a new report, the Starter 401(k) could help up to 19 million American workers participate in a workplace-based retirement plan. The report also estimates a 22% increase in retirement plan access for Black and Hispanic American workers.

How does a Starter 401(k) plan work?

Starter 401(k)s are exempt from IRS nondiscrimination testing, but the streamlined compliance means there are more strict requirements, including:

- Employers can’t contribute.

- Employee contributions can be no more than $6,000 per year starting in 2024, the first year the plans will be available. After that, the contribution level may be adjusted each year.

- Employees over 50 can contribute an additional $1,000 in catch-up contributions for a total limit of $7,000 in 2024.

- Employees are automatically enrolled at a contribution set by the plan sponsor of at least 3% and no more than 15% of their salary.

Who can open a Starter 401(k)?

Starter 401(k) plans can start as early as January 1, 2024. Employers are only eligible for a Starter 401(k) if they don't yet provide their workers with a retirement plan. But there are a few exceptions:

- Businesses that previously had an IRA through a mandated state-sponsored retirement program can choose to convert their plan to a Starter 401(k).

- If a company previously offered a 401(k), but they terminated it and have not offered any retirement plan in at least 12 months, they may be eligible for a Starter 401(k).

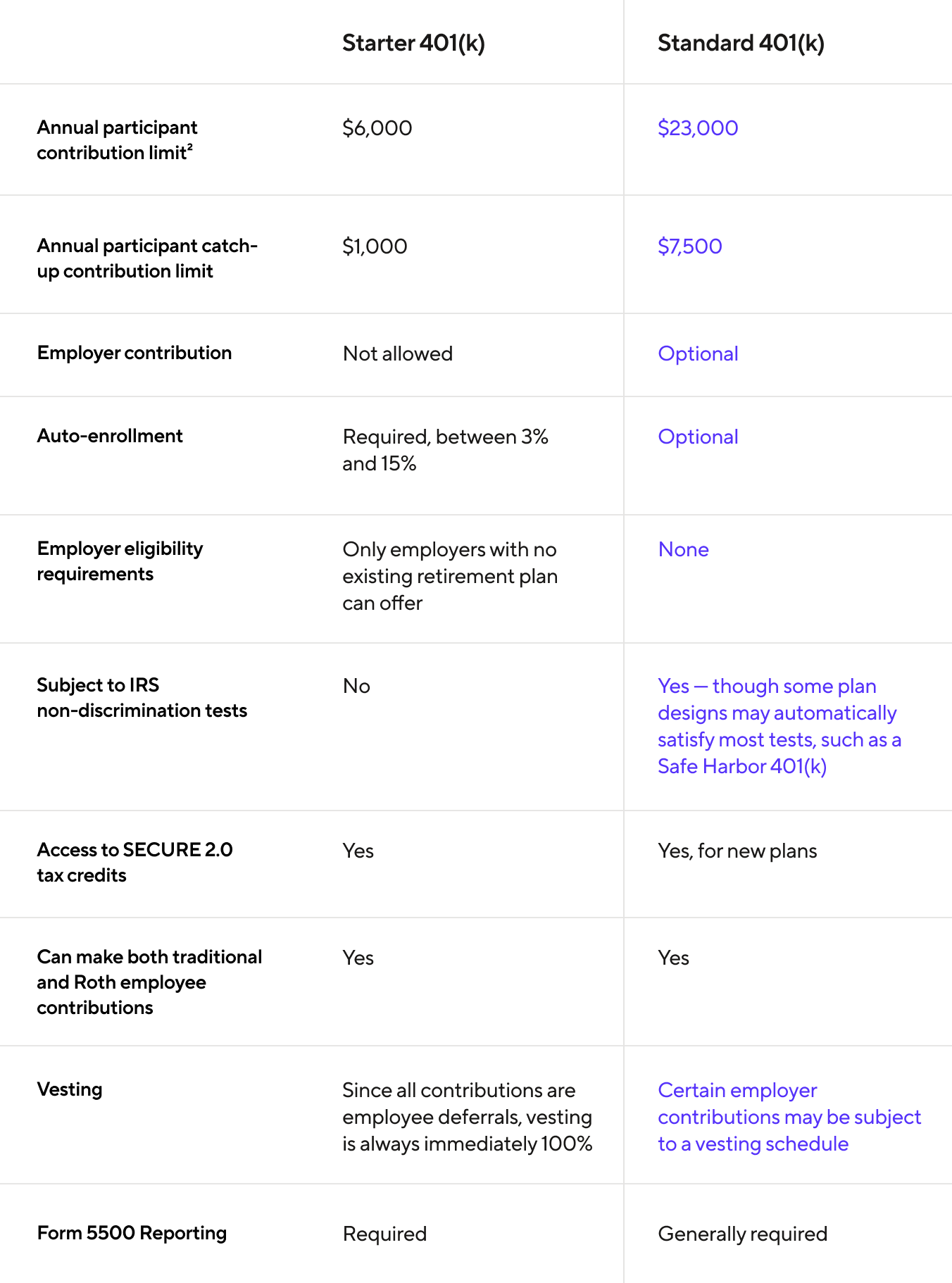

Starter 401(k) vs. Standard 401(k)

From cost to flexibility, there are significant differences between a Starter and standard 401(k) that employers should be aware of. You may already be familiar with a standard 401(k), which has significantly higher contribution limits and allows employer contributions.

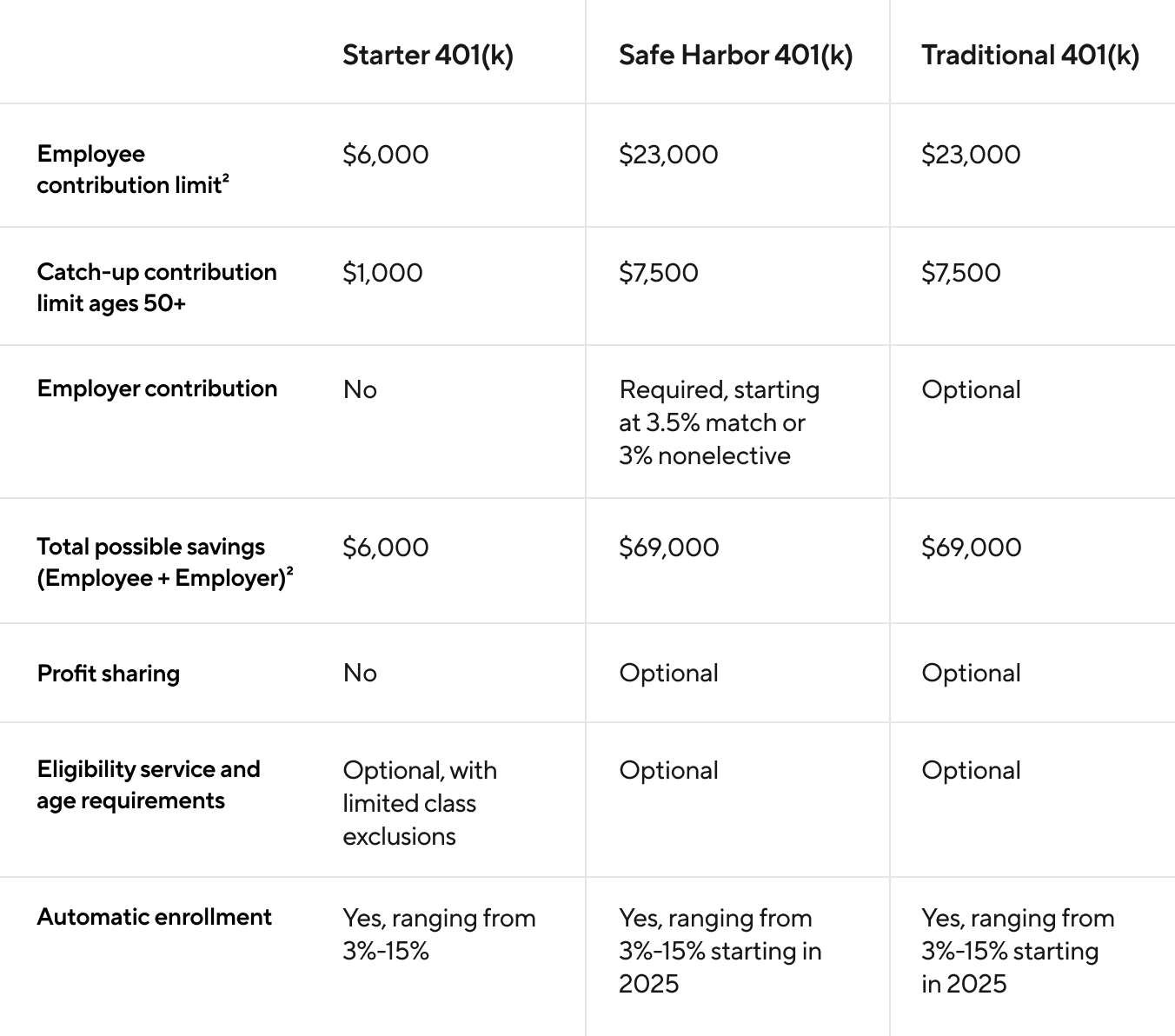

What's the difference between a Starter 401(k) and a Safe Harbor 401(k)?

There are similar benefits to Starter and Safe Harbor 401(k) plans regarding nondiscrimination compliance tests. But Starter 401(k) plans have more limitations.

Unlike a Safe Harbor 401(k), with a Starter 401(k), employers can not contribute to their employees’ savings. The contribution limits are also lower with Starter 401(k) than with a Safe Harbor 401(k) plan. The chart below breaks down the differences.

What's the difference between a Starter 401(k) and traditional no-match 401(k)?

Starter 401(k)s have many differences compared to a traditional 401(k), including lower contribution and catch-up contribution limits, no employer contribution match, and automatic enrollment. In order to offer a 401(k) without a match, you’ll be setting up a traditional 401(k), which will be subject to annual non-discrimination tests. See the chart below for details.

Starter 401(k) benefits

Starter 401(k) plans offer employers great advantages, including:

- Low cost and simplified administration: Starter 401(k) can be cheaper and easier to administer than standard 401(k) plans. Since they’re exempt from IRS testing, they don’t require the same amount of valuable administrative resources as a standard 401(k).

- Automatic enrollment: The automatic enrollment of eligible employees in Starter 401(k) plans may increase employee participation, since employees don’t have to do anything to get started. Employees can opt out if they choose.

- Meets state mandate requirements: Businesses can choose to offer employees the mandated state-sponsored retirement program, or they can offer their own private 401(k), such as a Starter 401(k) plan.³

Starter 401(k) limitations

While a Starter 401(k) plan may be a good fit for many employers, they pose several limitations, including:

- Lower contribution limits: With a Starter 401(k), the annual employee contribution limit is $6,000 (for 2024), which is significantly lower than the standard 401(k) limit. That means employees have less tax-advantaged savings for retirement each year.

- No employer contributions: Employers are not allowed to contribute to employees' Starter 401(k) plans, even if they’d like to.

- No flexible plan design options: Starter 401(k) plans have a one-size-fits-all approach to retirement benefits. They aren't as flexible as standard 401(k)s, which offer elective benefits such as profit sharing, vesting, and expanded eligibility requirements.

Who might a Starter 401(k) be a good fit for?

Think your company might benefit from a Starter 401(k) plan? Here are a few reasons why you might choose to consider this new, streamlined retirement savings benefit:

- Employers looking for a fast, simple, budget-conscious 401(k) solution

- Employers wanting to avoid compliance testing

- Employers who don’t plan on contributing to their employees’ retirement savings

If you think a Starter 401(k) could be right for your business, Guideline can help you give your employees a road to retirement.⁴

¹ This content is for informational purposes only and is not intended to be taken as tax advice. You should consult a tax professional to determine what types of tax credits or deductions your company is eligible to claim.

² Starter 401(k) and Standard 401(k) annual limits may be adjusted annually by the IRS to account for cost-of-living changes. Learn more.

³ This information is general in nature and is for informational purposes only. It should not be used as a substitute for specific tax, legal and/or financial advice that considers all relevant facts and circumstances. Deadlines, fees, and other program details are subject to change by the state without notice and should be checked prior to making any decisions.

⁴ Please note, under current IRS rules, Starter 401(k) plans can only be converted to full 401(k) plans effective the first day of the plan year. This would require you changing to the Core or Enterprise tier at the beginning of a calendar year.